MY INVESTMENT - NORTH LAS VEGAS, NV

A POST-CRISIS BUY IN NORTH LAS VEGAS - THE DEAL OF A LIFETIME, AND WHAT IT TAUGHT ME.

Estimated 27% IRR / x13.37 MOIC since purchase - but read why I don't try to repeat this.

This is one of my own personal investments - and it's an unusual one. I'm sharing it because the numbers are remarkable, but more importantly because of what it taught me about the difference between a great opportunity and a repeatable strategy.

In 2012, in the aftermath of the subprime mortgage crisis, I acquired a 3-bedroom, 2-bathroom, 2,100 sq. ft. home in North Las Vegas, NV (zip 89084) for $110,000. The property had originally sold for $340,000 in 2006, and had lost 65% of its value in the crash. The previous owner walked away. The bank foreclosed. I bought it for $110K - roughly what it cost to build.

The first tenant moved in shortly after at $1,295/month. By 2024, that rent had grown to $1,925/month.

THE BACKGROUND - TURNING CRISIS INTO INVESTMENT OPPORTUNITY

The subject property, constructed in 2006, reached an initial valuation of $340,000. Following the 2008–2009 subprime mortgage crisis, the local real estate market experienced significant contraction, resulting in a 65% depreciation of asset value. This volatility led to the abandonment of the asset by the original owner and a subsequent bank foreclosure.

The property was acquired as a distressed asset for $110,000, representing a substantial discount from both the original purchase price and the cost of construction. This entry point allowed for a low-capital market entry, mitigating the financial risks associated with the high-leverage environment typical of new developments.

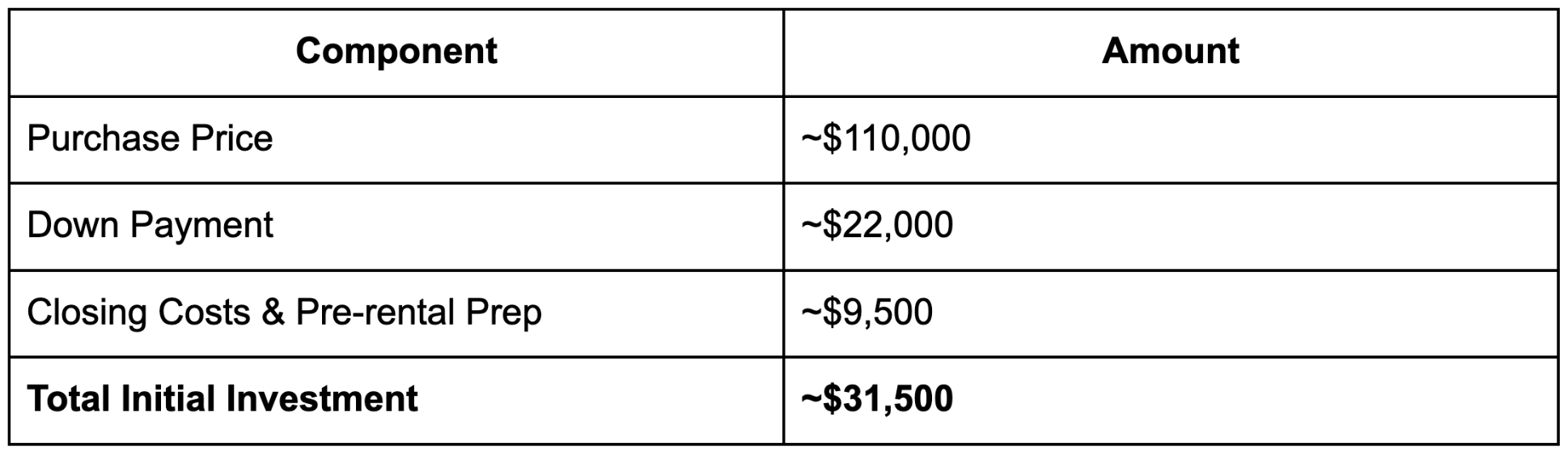

INITIAL INVESTMENT ENTRY

Financing 80% of the purchase, made the cash outlay relatively small, minimizing the exposure risk in a recovering market.

THE HONEST CONTEXT

27% IRR IS EXTRAORDINARY. HERE’S WHY IT’S NOT THE GOAL.

The returns on this investment are exceptional - but they were driven by a once-in-a-generation market dislocation. Buying a foreclosed property at 32 cents on the dollar, in a market that had just lost 65% of its value, is not a repeatable strategy. It requires perfect timing, distressed supply, and a willingness to take on risk that most investors shouldn't take on.

The North Las Vegas market also behaved differently from Knoxville in one important way: by 2024, the property's estimated value was only 18% above its original 2006 purchase price of $340,000. Twelve years of appreciation, and the underlying asset is barely above where it started. The returns came from the crisis entry point - not from the market itself.

This is why my conservative playbook - the one I use with clients today - is built around Knoxville-style markets: stable, education-driven, low-volatility, with strong rental yields. Markets where a 9% IRR is the floor, not the ceiling, and where you don't need to time a crisis to win.

THE COMEBACK

With one exception in 2014 - a vacancy and some appliance replacement costs - this property generated positive cash flow every single year for 12 years.

Total Rent Cashflow (2012-2024): $90,338

Accumulated Principal Payments (2018-2024): $23,044

Total Rental P&L Value: $113,382

Rental rates increased from a baseline of $1,295/month in 2012 to $1,925/month in 2024. This represents a Compound Annual Growth Rate (CAGR) of 3.7% in rental income, outpacing standard inflation hedges.

(1) RENTAL INCOME STORY

(2) WHAT THE PROPERTY IS WORTH TODAY

The timing of the acquisition during a period of market distress maximized the potential for capital gains. While the asset remains unrealized (unsold), current valuations indicate a substantial increase relative to the acquisition basis.

Purchase Price (2012): $110,000

Estimated Value (Late 2024): ~$425,000

Average Annual Appreciation (CAGR): ~11%

The initial investment hypothesis - projecting a full value recovery - was validated, though the timeline to parity extended to eight years, slightly beyond the original seven-year forecast.

(3) THE VOLATILITY CAVEAT - WORTH UNDERSTANDING

Analysis of the long-term price trajectory reveals that the 2024 estimated value is only 18% higher than the original 2006 purchase price of $340,000.

This suggests that while the North Las Vegas submarket offers strong yield potential through rental income, the underlying asset value remains subject to high volatility, where significant appreciation is largely dependent on timing the market cycle correctly rather than linear growth.

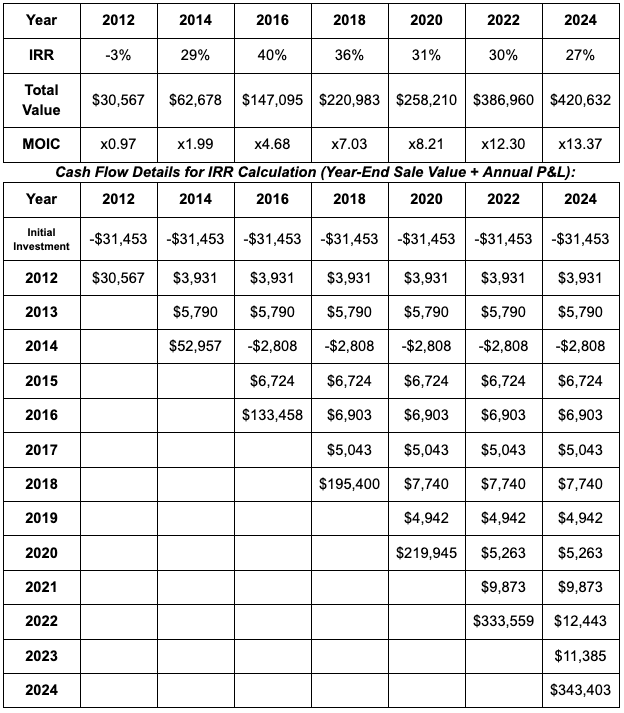

PUTTING IT TOGETHER: 27% IRR OVER 12 YEARS.

Combining consistent rental income with the dramatic appreciation from the crisis entry point, this investment delivered an average annual IRR of 27% between 2012 and 2024. An initial investment of ~$31,500 grew to an estimated value of ~$343,000.

Extraordinary - and unlikely to be repeated in normal market conditions. Which is exactly why I built a different playbook for my clients.

THE FULL PICTURE - YEAR BY YEAR

Here's every year, including the ones that were flat or negative. No editing.

Internal Rate of Return (IRR) by Holding Period

This table shows the IRR achieved if the property were sold at estimated value (minus cost of sale) at the end of each respective year, based on a constant initial investment of -$31,453:

INTERESTED IN WHAT A CONSERVATIVE, REPEATABLE VERSION OF THIS LOOKS LIKE?

The North Las Vegas story is a great one - but it's not the blueprint. The Knoxville case study is. If you want to understand what a disciplined, long-term investment looks like in a stable market, that's where I'd point you first.

→ See the Knoxville case study - the conservative playbook in action